Aggregate Supply(AS): The level of real GDP (GDPᵣ) that firms will produce

Long Run vs. Short Run

Long Run vs. Short Run

Long Run

- The period of time where input prices are completely flexible and adjust to changes in the price level.

- In the long run, the level of real GDP supplied is independent of the price level.

- The period of time where input prices are sticky and don't adjust to changes in the price level.

- In the short-run, the level of real GDP supplied is directly related to the price level.

Two Types of Aggregate Supply

Long-run aggregate supply (LRAS)

- Marks the level of full employment in the economy (analogous to PPC)

- Because input prices are completely flexible in the long-run, changes in price level don't change firms' real profits and therefore don't change firms' level of output.

- This means that the LRAS is vertical at the economy's level of full employment.

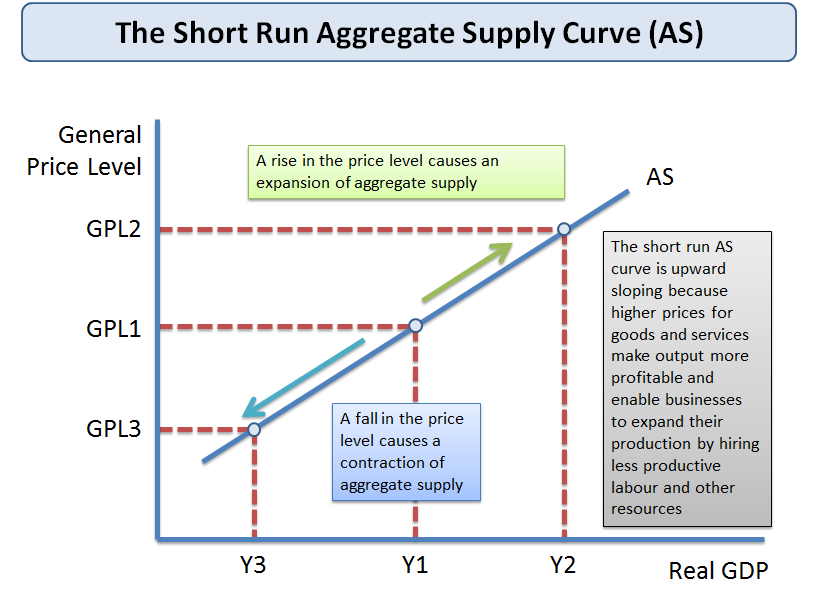

Short Run Aggregate Supply (SRAS)

Happens because input prices are sticky in the short-run, the SRAS is upward sloping.

Changes in SRAS

- An increase in SRAS is seen as a shift to the right (SRAS →)

- A decrease in SRAS is seen as a shift to the left (SRAS ←)

- The key to understanding shifts in SRAS is the per-unit cost of production.

Per unit production cost = (total input cost)/(total output)

Determinants of SRAS

1. Input/resource prices

- Domestic resource prices

- Wages (75% of all business costs)

- Cost of capital

- Raw materials (commodity prices)

- Foreign resource prices

- Strong dollar (appreciation) = lower foreign resource prices

- Weak dollar (depreciation) = higher foreign resource prices

- Market power

- Monopolies and cartels that control resources and control the price of those resources

Increases in resource prices = SRAS ←

Decreases in resource prices = SRAS→

2. Productivity

- Calculate using (Total output)/(total input)

More productivity = lower unit production cost = SRAS→

Lower productivity = higher unit production cost = SRAS ←

Lower productivity = higher unit production cost = SRAS ←

3. Legal Institutional Environment:

- Taxes and subsidies

- Taxes (money the government receives) on businesses increase per-unit production cost = SRAS←

- Subsidies (money the government gives) to businesses reduce per-unit production cost = SRAS→

- Government regulation

- Government regulation creates a cost of compliances = SRAS←

- Deregulation reduces compliance costs = SRAS→

No comments:

Post a Comment